Articles

Key Insights

- Credit card platforms cannot rely on a single data standard. Sustainable architecture requires intentional layering across messaging, settlement, governance, and semantic domains.

- Credit card industry data standards ISO 8583, ISO 20022, BIAN, and FIBO do not compete. They operate at different architectural layers and deliver distinct value.

- Institutions that attempt to consolidate standards into one universal model introduce operational risk and regulatory exposure.

- Semantic consistency across operational systems and analytics platforms is now critical for explainable AI and model governance.

Financial institutions increasingly compete on data, analytics, and trust. Nowhere is this more evident than in credit card platforms, where real-time authorization, risk modeling, and regulatory reporting. And customer experience converges.

In a previous article in this series, I reviewed the high complexity of data standards in the Life Sciences industry. At least eight reference models cover the information domains used by life sciences organizations [1]. This paper posited that there is no single silver-bullet reference data architecture for Life Sciences. Each data and process standard, in whole or in part, plays a role in these organizations’ data strategies.

The same is true for financial services.[2]

As we noted, modern financial institutions increasingly compete on intangible assets—data, analytics, algorithms, and trust. Credit card data is among the most valuable of these assets, supporting security, fraud detection, risk modeling, personalization, pricing, and regulatory compliance.

Credit cards sit at the intersection of payments, lending, risk management, and customer experience. The credit card industry generates enormous profits for credit card banks and card networks, processes transaction data in real time, and faces intense regulatory scrutiny. At the same time, they remain among the most profitable product lines for banks and payment networks, generating revenue through interest, interchange, fees, and merchant services [2-4].

Financial Services Reference Architectures

A reference architecture is a reusable blueprint that defines the major systems, layers, and data flows that underpin an organization’s information processing. It specifies control points, data ownership boundaries, and governance responsibilities while remaining technology- and vendor-neutral. [3]

Several open architecture standards exist to address the complexities of data processing and management in the financial services industry, particularly in credit card processing. In this article, we focus on several of these standards, which are the most widely accepted in credit card processing.

Ontologies and Data Models

Ontologies are formal representations of meaning within a domain. They define concepts, relationships, and constraints so that systems share a consistent understanding of data. In credit card systems, ontologies ensure that terms such as transaction, fee, balance, and dispute mean the same thing across authorization engines, ledgers, analytics platforms, and regulatory reports.

Open Credit Card Data Models

In practice, no single data model is sufficient to support the full lifecycle of credit card data. The credit card industry relies on a layered set of open, public standards rather than a single monolithic data model, and these standards are central to modern credit card data architecture.

Layering the Standards

Layering refers to the intentional use of multiple, complementary data models and standards, each applied at the architectural layer where it delivers the greatest value. Rather than forcing a single model to serve all purposes, layering recognizes that real-time transaction processing, settlement and reporting, enterprise governance, and analytics each have distinct requirements.

Layering is a core concept across all reference architectures. In a complex industry such as Financial Services, no single comprehensive standard meets all data management requirements. Multiple standards complement one another to address distinct areas of business operations. [4]

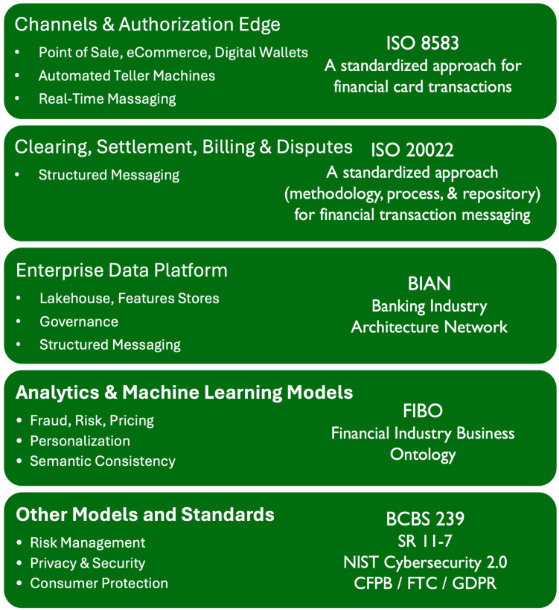

In practice, the credit card stack can be viewed as multiple abstractions over the same events:

- ISO 8583 operates at the event-transport layer: fast, minimal, schema-fixed messages optimized for real-time decision latency.

- ISO 20022 operates at the structured reporting layer: richer typing and feature space suited to aggregation, reconciliation, and regulatory reporting.

- BIAN operates at the system boundary layer, defining which services produce, own, and consume specific data objects.

- FIBO operates at the semantic layer: ensuring features, labels, and entities mean the same thing across models, time windows, and platforms.

- Other privacy and security standards (BCBS 239, SR 11-7, NIST Cybersecurity 2.0, CFPB/FTC/GDPR) also inform the architecture’s design and implementation.

The credit card industry, for example, relies on these standards to enable interoperable software for processing credit card transactions globally. There is no single monolithic data or process model. Figure 1 below presents a taxonomy of these standards.

Reference Architectural Models

ISO 8583

ISO 8583 remains the most widely adopted standard for card authorization and response messaging. At the transaction edge, ISO 8583 dominates because it is optimized for low-latency authorization and interchange messaging. It is compact, performant, and deeply embedded in global card networks. Attempting to replace ISO 8583 at this layer would introduce unnecessary complexity and operational risk. In practice, ISO 8583 has the broadest operational adoption across the credit card industry, embedded in every major network and issuer platform.

ISO 20022

ISO 20022, a global and open standard for information exchange, is adopted by a growing number of organizations across various domains, including:

- Securities

- Payments

- Foreign exchange

- Credit cards and related services, notably for end-to-end straight-through processing (STP)

- Regulatory reporting

ISO 20022 is increasingly becoming the preferred standard for settlement, reconciliation, and reporting. Its richer semantic structure improves regulatory reporting, cross-border payments, and integration with broader banking platforms. ISO 20022 complements ISO 8583; it does not replace it. [5]

BIAN

BIAN’s goal is to establish a common framework for banking interoperability and position BIAN as a world-class reference point for interoperability in the financial services industry. BIAN provides a capability-based reference architecture for banking services. Above these messaging standards, BIAN provides a service-domain and capability-oriented view of banking operations. This architectural layer clarifies system boundaries, data object ownership, and control points, making it particularly valuable during platform modernization and FinTech integration. BIAN is widely used as an architectural framework in large-bank modernization initiatives. BIAN is also used to future-proof applications and facilitate migration, improving system interoperability.[6]

FIBO

The Financial Industry Business Ontology (FIBO) provides a semantic foundation for enterprise data consistency. FIBO defines sets of data objects of interest in financial business applications and how those objects relate to one another. In this way, FIBO gives meaning to any data (e.g., spreadsheets, relational databases, XML documents) that describes the business of finance. FIBO provides the semantic foundation, offering a set of stable definitions of financial services across all layers. FIBO ensures that concepts such as transactions, fees, balances, and interest are defined consistently across operational systems, data platforms, analytics, and regulatory reporting. FIBO has the deepest semantic adoption for governance, analytics, and regulatory alignment.

Other Models and Standards – Risk Management, Privacy and Security

Other models and regulatory requirements should be factored into any comprehensive reference architecture for the financial services industry, including credit card organizations. These models and regulations focus on risk management, privacy, and security. A robust architectural framework enables earlier detection of emerging risks, strengthens supervisory oversight, and improves a bank’s ability to restore financial viability under stress, including by facilitating strategic alternatives such as mergers or orderly resolution.

BCBS 239 – Risk Data Aggregation and Reporting

BCBS 239 establishes expectations for the accurate, timely, and comprehensive aggregation of risk data across the enterprise. It emphasizes strong governance, consistent data definitions, and the ability to produce consolidated risk views under stress.

Architecturally, BCBS 239 requires traceable data lineage, controlled aggregation processes, and reliable enterprise reporting layers. Institutions that lack architectural alignment across transactional, risk, and reporting systems struggle to meet these standards, particularly during periods of financial or operational stress. Enhanced risk data aggregation significantly improves risk management, particularly for G-SIBs (Global Systemically Important Banks)—large, highly interconnected financial institutions whose failure could pose significant systemic risk to the global financial system, and which are therefore subject to heightened regulatory standards.

Resolution authorities must have access to comprehensive, accurate, timely, and adaptable aggregate risk data aligned with the FSB (Financial Stability Board)—the international body that coordinates global financial regulation and sets policy frameworks, including the Key Attributes of Effective Resolution Regimes for Financial Institutions.[7]

SR 11-7 – Model Risk Management

SR 11-7 outlines supervisory expectations for model governance, validation, and oversight. It applies to models used in credit risk, valuation, stress testing, compliance, and strategic decision-making.

SR 11-7 mandates clear data inputs, documented transformation logic, reproducible outputs, and independent validation controls. Poorly managed data architectures increase model risk by creating ambiguity in definitions, feature creation, and reporting outputs. A layered architecture with strong semantic alignment reduces this risk and enhances regulatory resilience.

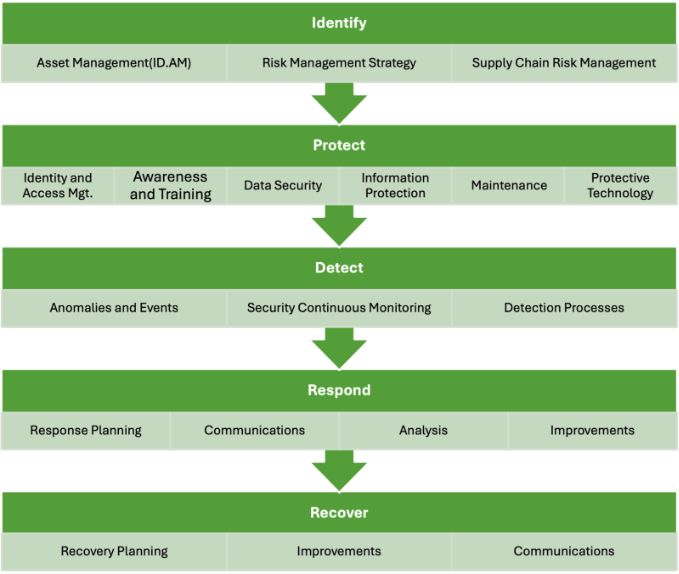

NIST Cybersecurity Framework 2.0

The NIST Cybersecurity Framework provides a comprehensive guide for organizations to develop and implement effective cybersecurity policies and practices. The NIST Cybersecurity Framework is not just one standard but an amalgam of many standards and guidelines covering multiple cybersecurity domains. See Figure 2. [8]

Consumer Protection (CFPB / FTC / GDPR)

Consumer protection in financial services encompasses regulatory obligations to ensure fairness, transparency, and accountability in the design, marketing, and servicing of consumer products. In the United States, the Consumer Financial Protection Bureau enforces prohibitions against unfair, deceptive, or abusive acts or practices (UDAAP) under the Dodd-Frank Wall Street Reform and Consumer Protection Act, with a focus on financial products such as credit cards. [9] The Federal Trade Commission, under the Federal Trade Commission Act, broadly prohibits unfair or deceptive acts or practices (UDAP) across commerce, including misleading advertising, inadequate data security, and privacy violations. [10]

Together, these frameworks emphasize clear disclosures, fair billing and dispute resolution, responsible marketing, and protection against consumer harm.

In the European Union, consumer data protection is regulated by the General Data Protection Regulation (GDPR), which protects individuals’ personal data through principles like lawfulness, transparency, data minimization, integrity, and accountability. The GDPR also provides enforceable rights, including access, correction, erasure, data portability, and limits on automated decision-making. [11] For credit-card platforms and financial institutions, these regulations collectively require strong data governance, explainable algorithms, secure processing environments, and auditable controls to ensure both product fairness and the protection of personal data across different jurisdictions.

Conclusion

Credit card data architecture involves layering complementary models at the right level, rather than selecting a single standard: ISO 8583 for real-time transaction messaging, ISO 20022 for structured settlement and reporting, BIAN for architectural domain alignment, and FIBO for semantic consistency.

When integrated into a coherent reference architecture spanning channels, authorization, clearing and settlement, enterprise data platforms, and analytics, these models support each other rather than compete. ISO 8583 offers speed, ISO 20022 provides structure, BIAN ensures architectural discipline, and FIBO promotes shared understanding. Together, they reduce semantic ambiguity, speed up integration, and enhance explainability for regulators and customers.

This layered approach enhances governance, risk management, and regulatory readiness while supporting modernization. For analytics and machine learning, it minimizes feature drift, label inconsistency, and training–serving skew, enabling data scientists to analyze transactions, balances, fees, disputes, and risk signals consistently across diverse systems.

By integrating these standards into a single reference architecture, financial institutions can expand and innovate without sacrificing control, auditability, or trust.

HOW GREEN LEAF CONSULTING GROUP ASSISTS FINANCIAL INSTITUTIONS

Green Leaf Consulting Group offers practical experience in helping financial organizations leverage data for risk management, customer analytics, digital transformation, strategic decision-making, and AI-driven innovation.

References

- Ferrara, E.,Data in the Evolving World of Life Sciences: Chaos to Order, inGreen Leaf Consulting Group – Insights, M. Miner, Editor. 2025, Green Leaf Consulting Group: https://greenleafgrp.com/insights/data-in-the-evolving-world-of-life-sciences-chaos-to-order/.

- Ferrara, E.,Why Data Now Defines Value in Banking and Financial Services, inGreen Leaf Insights, M. Miner, Editor. 2025, Green Leaf Consulting Group: https://greenleafgrp.com/insights/why-data-now-defines-value-in-banking-and-financial-services/.

- Systems, B.What is a Reference Architecture?2025; Available from: https://www.baesystems.com/en-us/definition/what-is-a-reference-architecture.

- Practice, L.Layered Enterprise Architecture. 2025 [cited 2026 February 17]; Available from:https://www.leadingpractice.com/enterprise-standards/enterprise-architecture/layered-enterprise-architecture/.

- Bank, F.C.,ISO 20022 What is it and how does it impact your business?, inTreasury Management. 2025, First Citizen’s Bank: https://www.firstcitizens.com/commercial/insights/treasury-management/iso-20022-definition-business-impact.

- (BIAN), B.I.A.N.BIAN – the Banking Industry Architecture Network. 2025 [cited 2026 February 17]; Available from:https://bian.org/deliverables/.

- Adachi, M., et al.,Basel Committee on Banking Supervision: Principles for Effective Risk Data Aggregation and Risk Reporting. 2013, Bank for International Settlements:https://www.bis.org/publ/bcbs239.pdf.

- NIST,NIST 800-12: Special Publication – An Introduction to Computer Security – The NIST Handbook, D.o. Commerce, Editor. 1995, National Institute of Standards: Washington, DC USA.

- Congress, t.U.S.,Public Law 111-203: Dodd-Frank Wall Street Reform and Consumer Protection Act, t.U.S. Congress, Editor. 2010, 111th Unitef States Congress: Washington, DC.

- Commission, F.T.,Dodd-Frank Wall Street Reform and Consumer Protection Act, Titles X and XIVF.T. Commission, Editor. 2010, Federal Trade Commission: Washington, DC.